Hi friends,

I was on holidays with the family last week. My ego likes to think you missed me…

You did miss me right??

Anyway…

I’m back in action and super excited to share this special piece with you, a Deep-Dive on the UK Mental Health Market.

For this article, I’ve teamed up with the truly wonderful Ushma Baros. Ushma is the Commercial Director at Big Health, the company behind products like Sleepio, Daylight and Spark. She is also an elected Governor at Central North West London NHS Foundation Trust.

Ushma has spent a large chunk of her career operating in the UK mental health system and understands it FAR better than I do. I learned so much from her when working on this piece and owe her all the credit and a huge amount of thanks.

Our goal with this piece was to create a guide to the UK market that would be helpful for mental health founders and operators. We had so much to share that we actually split it up into two parts, with Part II being released in the coming weeks.

Today, in Part I, we will cover;

The size of the prize: How big is the UK mental health market, where is the money spent and who are the biggest payers

NHS breakdown: What you need to know about the NHS and how it delivers mental healthcare

Commercialisation opportunities: Five opportunities for entering the UK mental health market (including several examples)

Regulatory overview: A very brief overview of the regulatory landscape in the UK, what you need to be aware of and our advice for anyone considering operating in this market.

MH Founder and Operator Survey

Before we get into the meat of today’s post… Want to share your experience of the Mental Health industry in 2024?

I’m gathering insights from mental health founders and operators and would love your input. I want to hear what your experience has been in 2024 so would appreciate you providing your input this short survey?

THR Pro

The next THR Pro meet-up is happening on December 17th. If you’d like an invite, consider becoming a THR Pro member.

As a member, you’ll also get access to additional insights and data each month, including my most recent deep-dive on The Eight Major Trends Shaping the Mental Health Tech Industry in 2024.

A Guide to the UK Mental Health Market (Part I)

Firs things first. If you’re considering tackling the UK mental health market, the first thing you need to know is the size of the market. How much money is spent on mental health each year and where is it spent?

So that’s exactly where we are going to start!

Size of the prize and market breakdown:

You’d think this would be an easy thing to find… wrong.

It’s actually very difficult to get these numbers.

To get to a number, we spent some time analysing a few different sources and where precise data was not available we made some reasonable assumptions.

Here’s what you need to know:

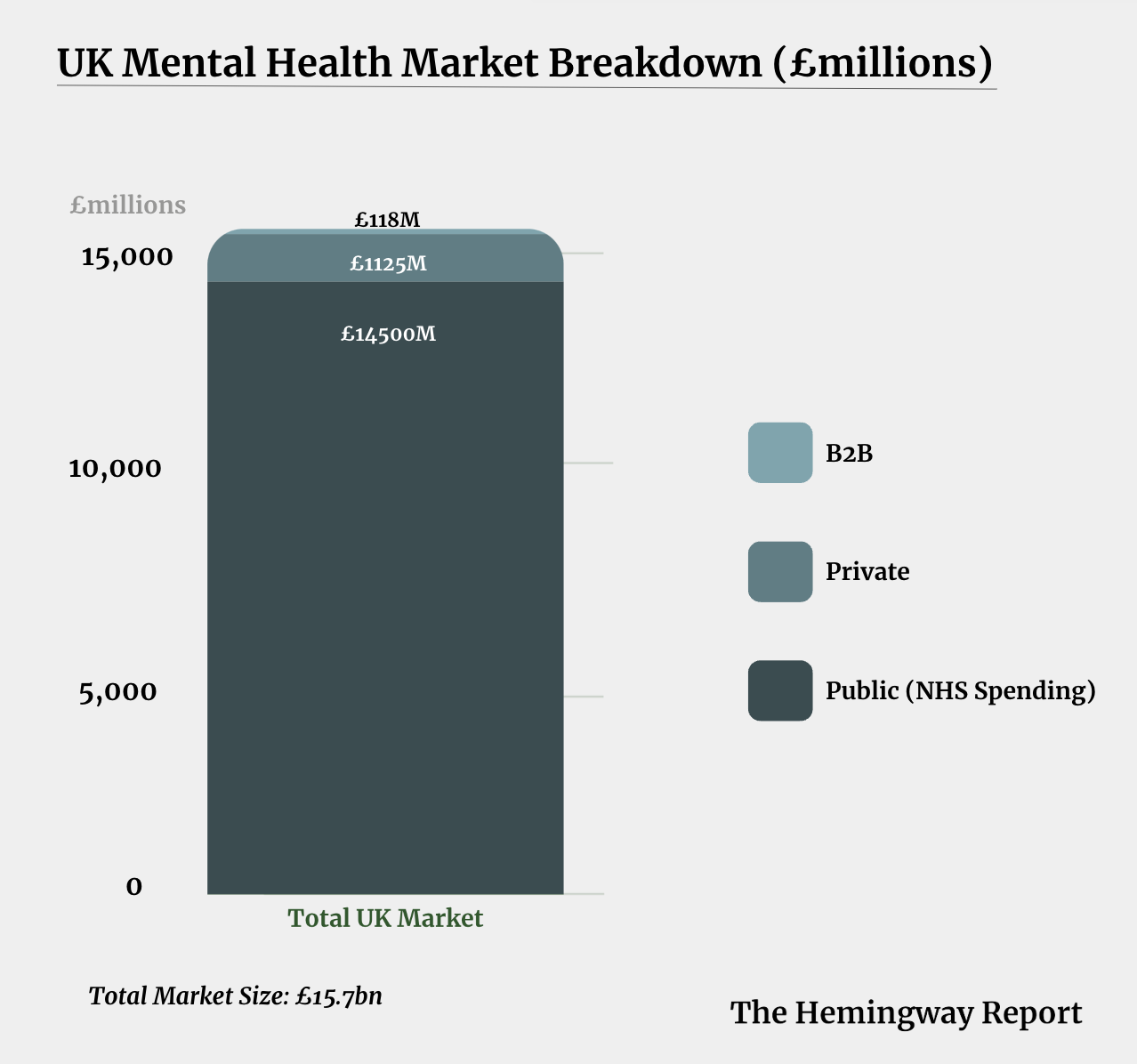

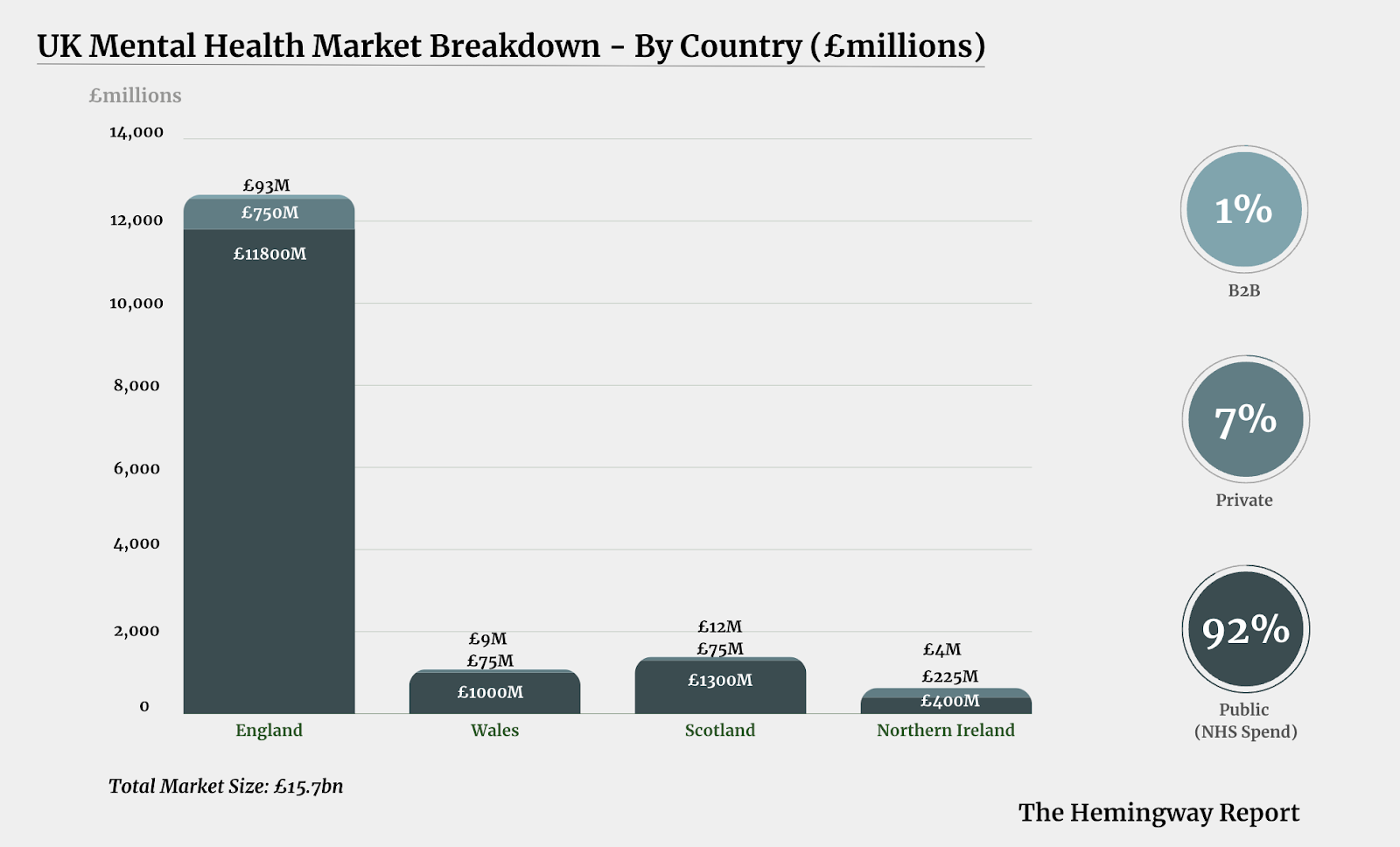

We estimate the total UK mental health market at £15.6bn*

The NHS is by far the biggest payer, accounting for 93% of all mental health spend.

While the UK comprises four separate countries, the majority (81%) of the market is in England.

Even though the NHS is the ultimate payer, they often pay private businesses to deliver mental health services. Overall, it’s estimated that 17% of NHS England’s spend on mental health services went to non-NHS providers in 2021-22. In addition, approximately 38% of the mental health hospital system is run by private businesses.

Private and B2B markets are relatively small (£1bn and £118m respectively)

*Note: for this estimate, we’ve focused on available public and private spend that we think is relevant for mental health tech businesses, largely the money spent on mental healthcare. We have excluded expenditure on things like welfare payments for people out of work due to poor mental health. This expenditure is a huge cost to the UK each year (an additional £13bn), but is not directly relevant to most mental health business.

The NHS is by far the biggest spender

England accounts for >80% of the total UK market

NHS Spend Breakdown

The NHS is the biggest market opportunity for any mental health business. So how do they spend their money? What types of services do they deliver and how much do they spend on each one?

The best and most relevant data is for NHS England, so let’s take a look at that.

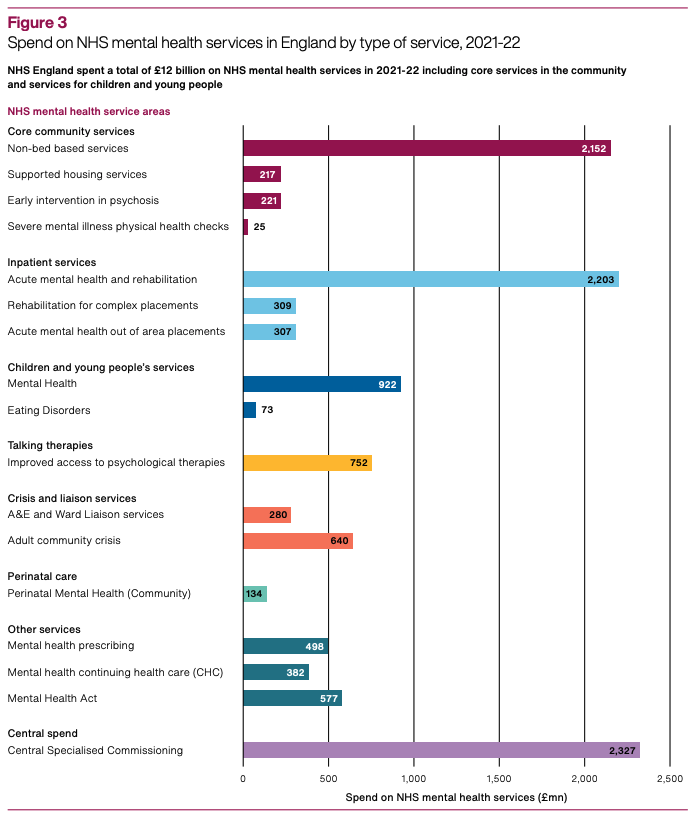

In 2021/2022 (the latest year for which we have good data) the biggest areas of spend were;

Central Specialised commissioning (national scale spending): £2.3bn

Non-bed based community mental health services: £2.2bn

Acute mental health and rehabilitation inpatient services: £2.2bn

Mental Health Services for Children and Young People (aka CAMHS): £900m

Talking Therapies (a national program to deliver psychological therapies for common mental disorders): £750m

This chart breaks it down in more detail…

NHS England Mental Health Spend by Service 2021-2022

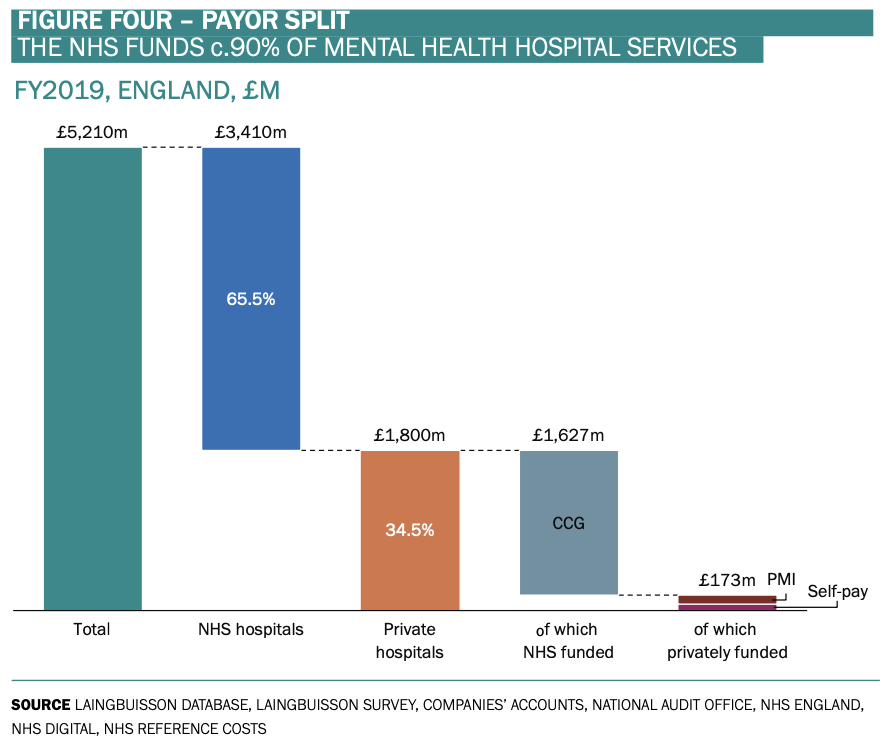

Even though the NHS is the end payer in this market, they often pay private businesses to deliver mental health services. For example, in 2019, £5.2bn was spent on mental health hospitals. £1.8bn (35% of that) went to private hospitals and 90% of that came directly from the NHS.

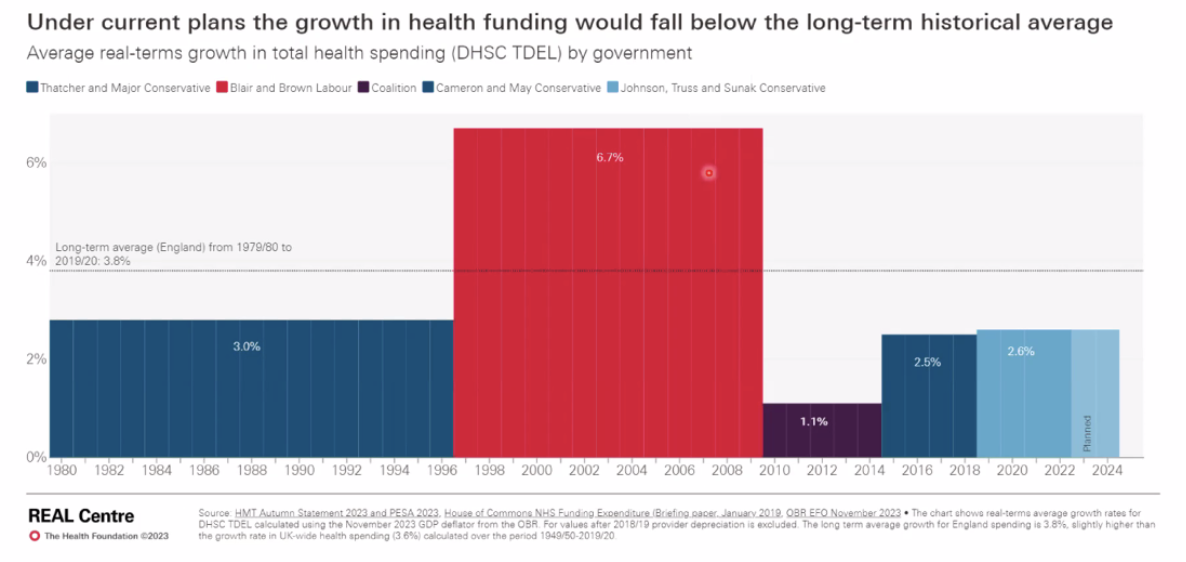

What about growth rates?

Between 2017/18 and 2022/23, total spending on mental health services went up by an average of 2.7% a year (in real terms). In the same period, spending on children and young people’s mental health increased by an average of 7% a year. Despite continued calls for increased spending, the level of increase in real spending has been limited and below the level needed to address some of the core challenges of the NHS

We really can’t understate the importance of the NHS in this market.

It accounts for the vast majority of spend and offers multiple commercialisation opportunities which we cover later in this piece.

So if you want to be successful in the UK market, you have to understand the NHS.

And that ain’t so easy…

Understanding the NHS

If you google “understanding the NHS”, this is what you’ll see.

At least they are self aware…

Here’s what you need to know about the NHS.

A brief history

The NHS was set up in 1948 as a core part of the new welfare state after the second world war. For the first time, healthcare was going to be free at the point of need for anyone who needed it, regardless of income.

The story of the NHS was, and continues to be, the story of the interactions between:

The people who need care (patients)

The people who deliver care (healthcare professionals), and

The people who fund care (the Government and, by extension, taxpayers)

We’ll come back to this tripartite a lot - it’s a helpful mental model for working with the NHS.

To be really clear - the NHS is how almost everyone in the UK gets their healthcare. It:

Treats 1.3m people a day - the equivalent of the entire population of Maine

Employs 1.5m people - making it one of the 10 largest employers in the world

Provides 227 meals a minute to patients, staff and visitors

The ‘National’ part of the NHS is a bit of a red herring. There are separately run systems in England, Wales, Scotland and Northern Ireland and within each nation most care is delivered by local bodies.

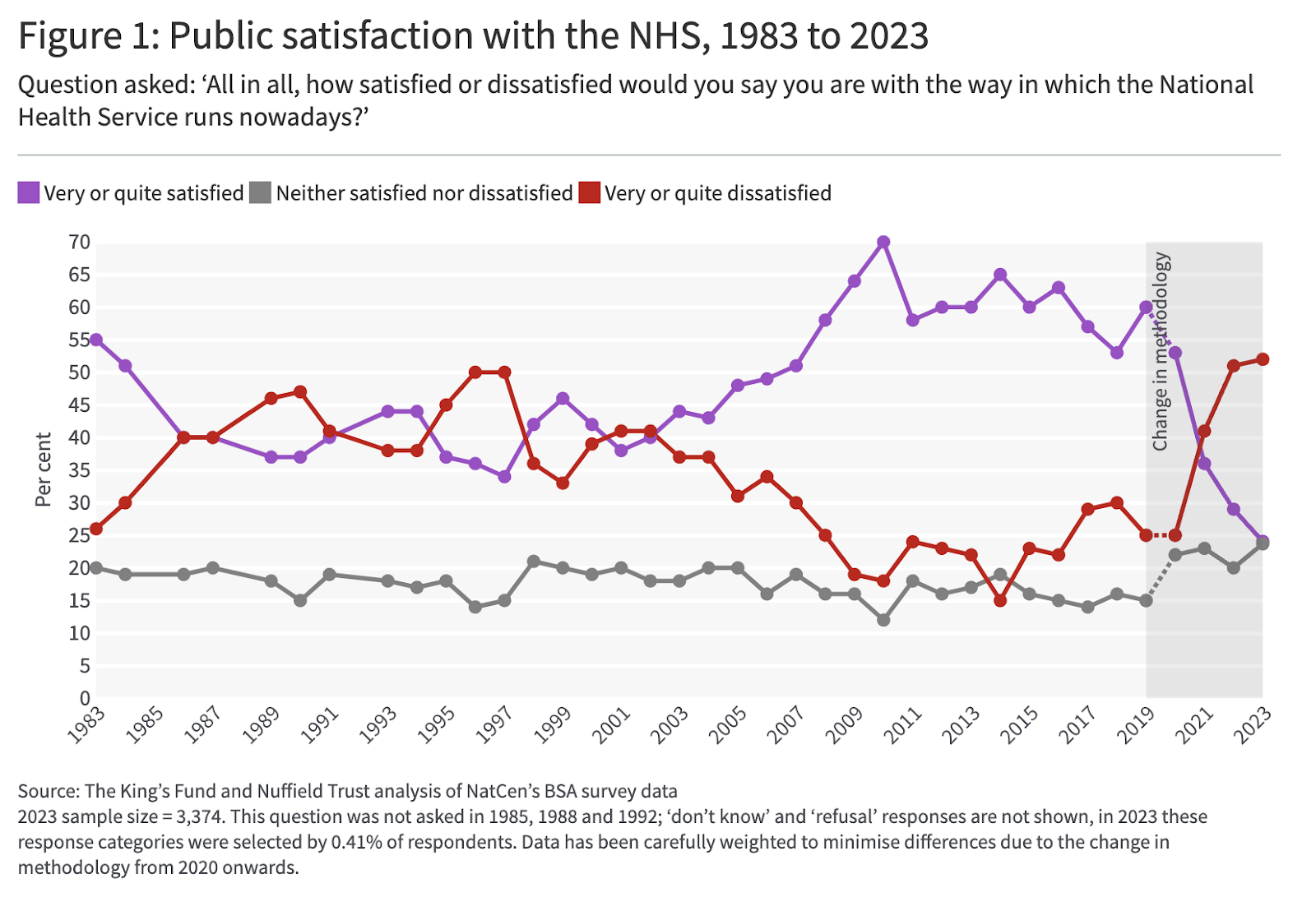

Public satisfaction with the NHS was historically high - the 2012 London Olympics opening ceremony included James Bond, the Queen, and… the NHS.

The NHS at the 2012 London Olympics

But survey data shows that satisfaction has been dropping dramatically post-COVID - in 2023, less than a quarter of the public say they are satisfied with the NHS overall.

From a mental health perspective - things seemed to be improving for a bit. In 2019, the government announced it would invest an extra £2.3bn in mental health services per year by 2023-24 as part of the Long Term Plan for Mental Health.

But demand rose faster than the growth in funding. There were an estimated 4.8m new referrals to mental health services in the UK in 2022-23, fifty per cent higher than in 2017-18. On top of the increase in demand, mental health faces some of the worst staffing shortages across the NHS. Thirty per cent of mental health nurses will approach retirement age in the next five years.

The disconnect between needs and the ability to meet them are a core driver of dissatisfaction with the NHS.

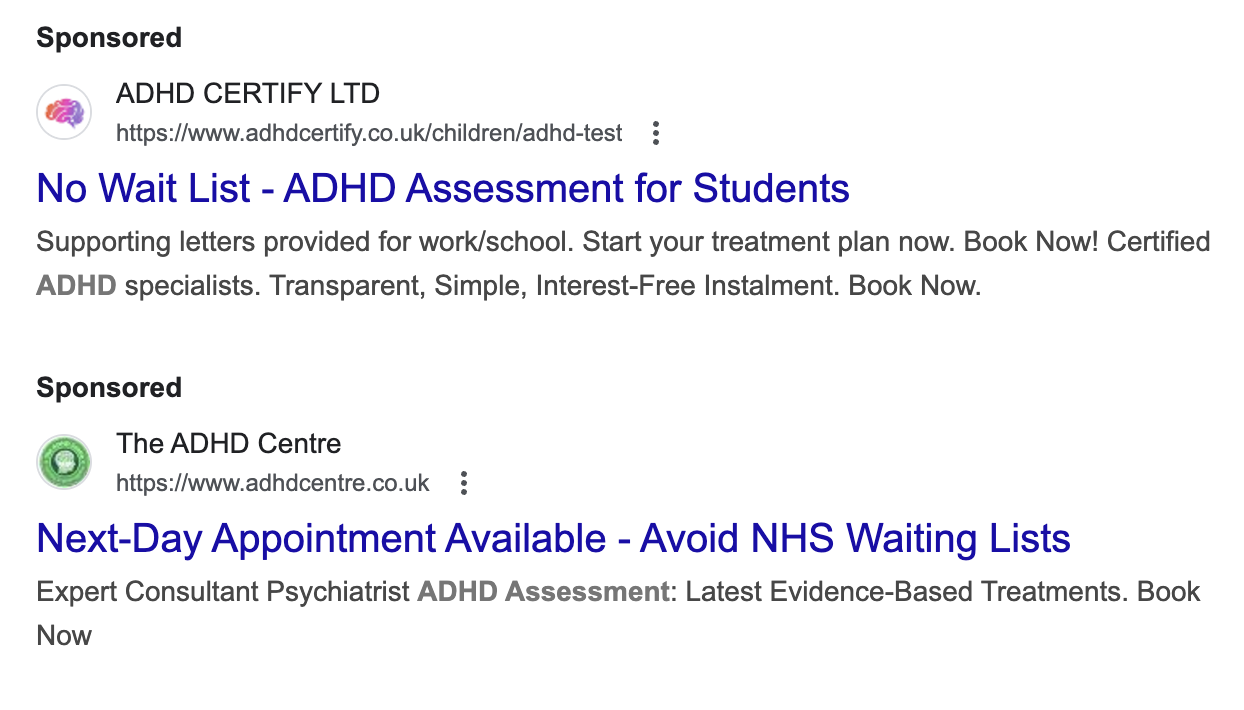

This manifests in a major waiting list problem - if you google ‘ADHD assessment NHS’ these are the first two results you get:

Technology can’t completely solve this demand and supply problems in the NHS. But mental health business can certainly help address this problem, and we’ll dive into that later.

How the NHS is structured

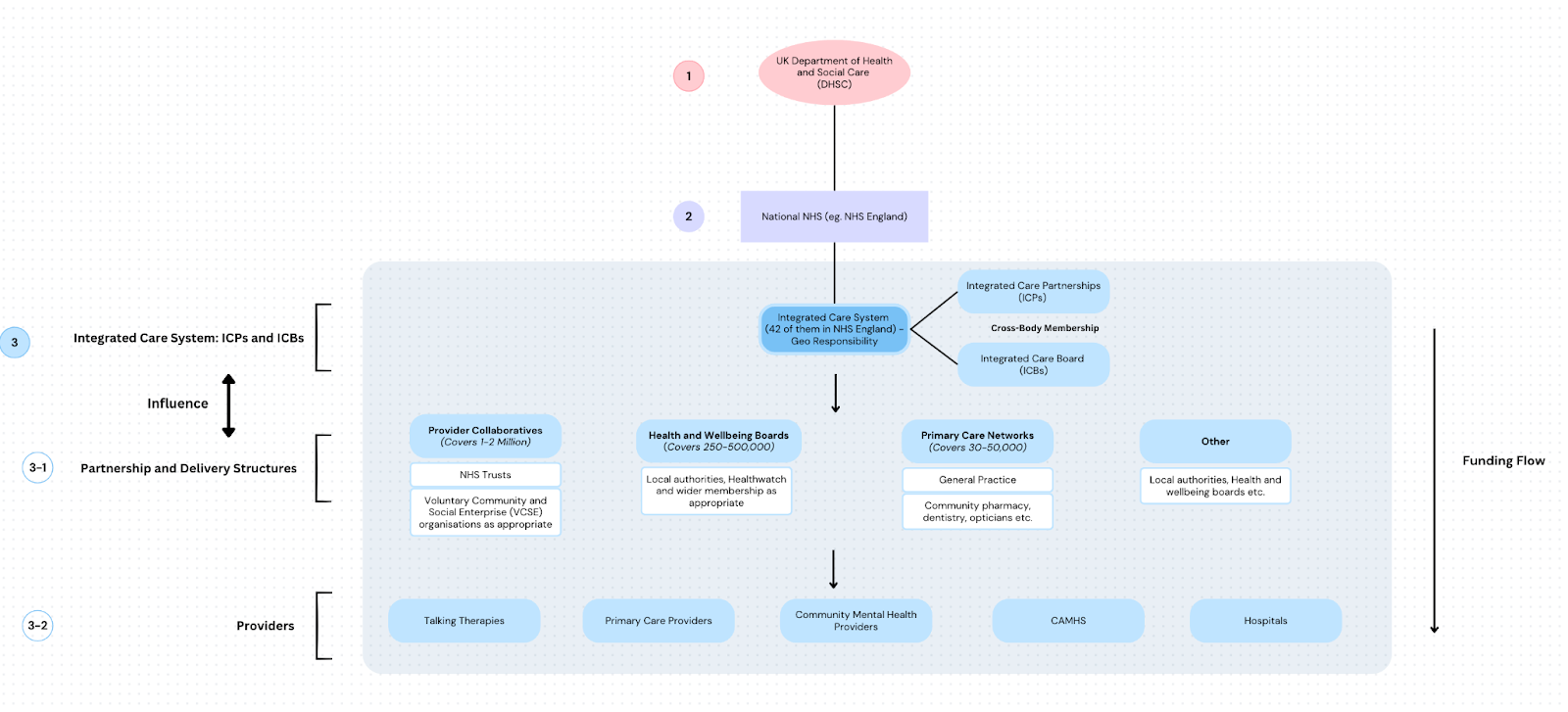

Now that you understand a little about the history of the NHS, it’s helpful to understand how actions, accountability and finances flow through the NHS when it comes to mental healthcare. This is super important to understand for anyone entering or operating in the market.

For the purpose of this article, we’ll focus on England, the largest market. The diagram below is illustrative, rather than exhaustive, but hopefully helps explain the flows of money and influence. Open it up to view it in more detail.

An illustration of the NHS Mental Health System

Let’s dig into each of these layers a little more and see what we can understand about how they run mental healthcare. Stick with us now!

Within the UK Government, the UK Department of Health and Social Care (DHSC) is responsible for setting the overall policy and funding allocations for the NHS, aligned with the Government’s political commitments to improving mental health care. The DHSC is accountable for:

Overall NHS performance

Mental health targets

NHS England, using this funding, is then responsible for setting and monitoring the overall strategy and national targets for mental health services in England, as well as overseeing specialised commissioning i.e. national-scale spending (in 2021/22 this spend was over £2bn out of a total of £12bn spent on mental health). NHS England is accountable for:

Delivering against the mental health investment standard i.e. the commitment to increase parity of investment in physical and mental health

Delivering against the Long Term Plan for Mental Health (until 2023/24)

Underneath NHS England there are 42 Integrated Care Systems. These bodies plan, allocate and ensure delivery of mental health services at a local level. These local systems - a partnership between the local NHS (confusingly, called ‘Integrated Care Boards’), social care, and local councils (i.e. the local Government), are required to:

Meet the Mental Health Investment Standard

Meet national targets for mental health service provision

Within the Integrated Care Boards there are 50 Mental Health Trusts. These trusts provide secondary mental health services in local areas, implement new care models and service improvements. Examples include Talking Therapies (psychological therapies for common mental disorders), specialised services for Child and Adolescent Mental Health (CAMHs), community mental health services, and teams aimed at specific groups or disorders. Incentives available include:

Commissioning for Quality and Innovation (CQUIN) schemes to improve specific aspects of care

Funding tied to meeting performance targets and service standards

Another part of Integrated Care Boards are Primary Care services which offer first-line mental health support and referrals, as well as participating in integrated care models for mental health. Financial incentives in primary care include:

Funding for additional mental health support roles

Local councils, part of the Integrated Care Partnerships, are also responsible for a number of factors linked to mental health and preventing poor mental health (housing, schools, green spaces etc.) and also have dedicated responsibilities, such as providing housing / social care for people experiencing poor mental health, or support for children and young people

Got it? Great!

Like most large public health systems, it’s not straightforward.

But hopefully you can return to this guide when you need it and use it to help navigate the NHS. We’ll make this more tangible below when we talk about some of the commercialisation options available to mental health businesses.

So you should know a bit about the NHS, how it spends its money and how it operates. But what direction is it heading and what do you need to know about how recent elections might change its trajectory?

A new government, a new NHS?

In July 2024, a Labour Government was elected after 14 years of its main opposition, the Conservatives. The two parties traditionally have different approaches to health spending, with Labour spending more than the Conservatives:

Labour Governments tend to spend more on healthcare

On his first day in office, the new Labour Secretary of State for Health, Wes Streeting, made the statement “From today, the policy of this department is that the NHS is broken”. He commissioned an independent review of the NHS in England and announced that they will deliver a new 10 year plan for the NHS in spring of 2025.

Despite the challenges that exist in the NHS - the Government and public are clear - they do not want a change to the principles of the NHS i.e. taxpayer funded, free at the point of use, and based on need not ability to pay. NHS workers are highly skilled, and values-driven. But there’s a growing acceptance that - like all systems facing growing healthcare costs and complexity - things need to be done differently.

There are three main shifts being discussed for the future of the NHS:

From analogue to digital

From treatment to prevention

From hospital to community

On the 30th of October the new UK Government announced their Budget. This included the largest increase in the NHS’ budget since 2010 (outside of COVID spend). But recent analysis from the Health Service Journal suggests that 2024/25 is looking like a very tight year despite this - of the c. £8bn going to NHS England, it’s estimated that £2.5bn will go to inflation and the rest likely to staff pay rises. In other words - that money is for business as usual, not something new.

The budget also received criticism for its lack of focus on mental health. If I were optimistic, I’d hope that more mental health announcements (particularly a renewal of the Government’s critical commitment to parity of investment in mental health) will be saved for the new NHS 10 Year Plan coming in the spring.

So, should you wait until this 10 Year Plan is published to do something in the UK market?

In short, no.

As we’ll get into in Chapter 2, entering the UK market is not a quick job, and even if there is something exciting announced next Spring, you’ll need to have developed relationships and have contacts on the ground to translate whether that’s actually exciting (i.e. creates budget relevant for you) in practice.

Commercialisation Options

OK, so now you know where the money is spent in the UK market and how the NHS is structured when it comes to the delivery of mental healthcare. This is a good start for understanding where you can target your commercialisation efforts - the bigger the pool of spend, the bigger the opportunity.

But spend only tells you part of the story. To understand the potential for you to succeed in the UK, you should also consider where there’s evidence of mental health companies succeeding.

Let’s understand a few of these areas better and the opportunities they present. We’ll look at;

NHS Talking Therapies

National services

Local NHS / Government

Selling to businesses

Going D2C

1. NHS Talking Therapies

Talking Therapies is a service in England that offers treatment for anxiety and depression, delivered by trained NHS practitioners, available for free on the NHS with or without a referral. We’ve called this out first in our list, not because of its size, but because it has been an early adopter of mental health tech in England, and there’s a path to scale for both treatments and platforms or services.

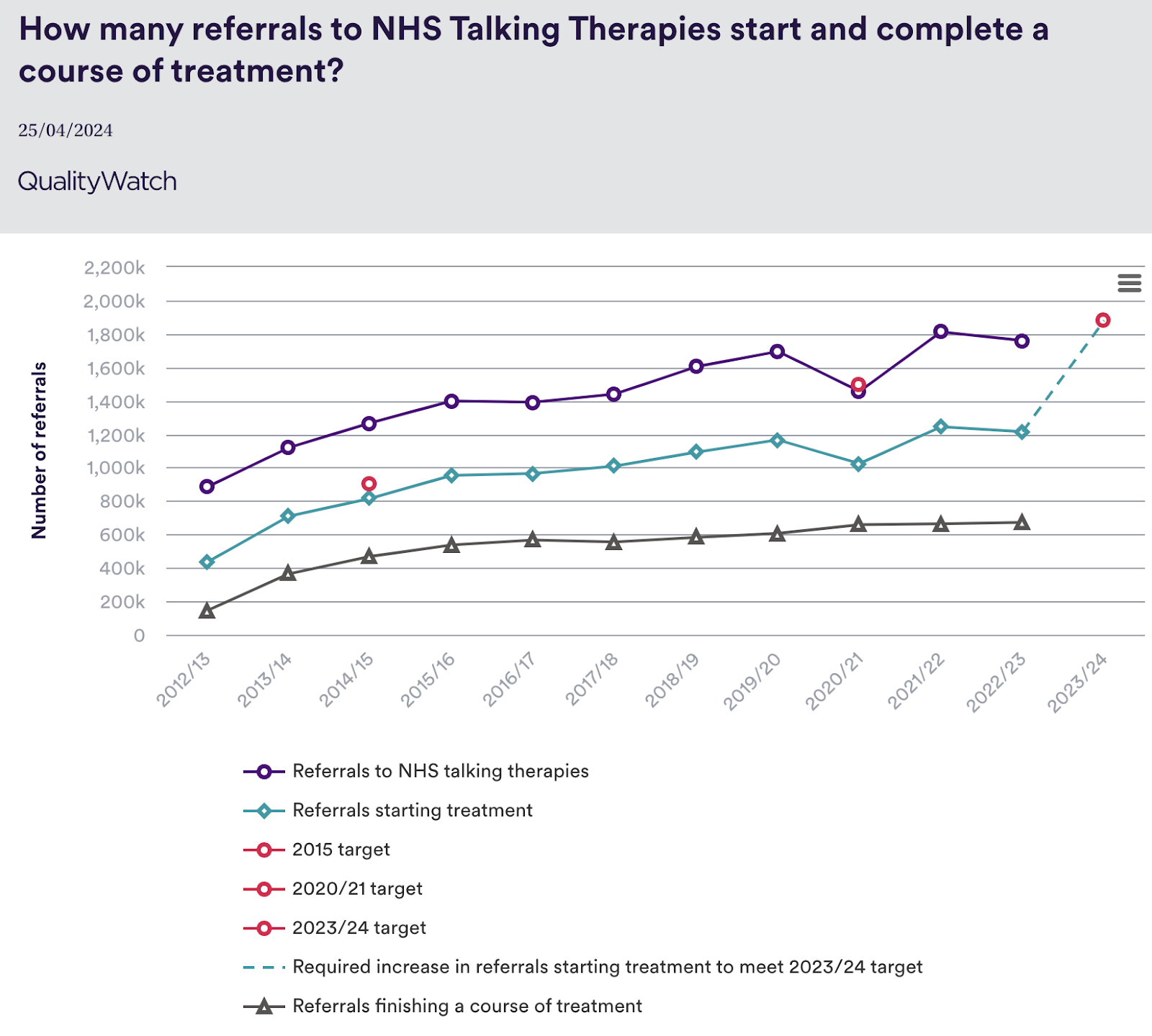

The NHS spend on talking therapies has grown significantly in recent years, reaching £911m in 2023/24.

The history of Talking Therapies (formerly known as IAPT) is actually a pretty interesting read - it involves a chance encounter at a British Academy Tea Party (I’m not making this up). The goal was to offer evidence-based treatment - largely, CBT for anxiety and depression - and collect data on its usage and outcomes. It was also claimed that getting these patients back to work, and off welfare payments, would cover the cost of training more therapists.

It was set up in 2008, aiming to reach 15% of patients with anxiety and depression.

Sixteen years later, the programme has grown considerably - in July 2024, there were 151,365 referrals to Talking Therapies, 108,738 patients accessing therapy, and 54,556 internet enabled therapy sessions took place.

There appears to be two routes to working with Talking Therapies services:

Sell a patient-facing technology that meets the relevant standards

Sell a service / platform that improves the efficiency of existing services

Patient Facing Technologies

Patient-facing technologies for Talking Therapies are called Digitally Enabled Technologies and have very strict criteria, mimicking the highly data-driven nature of the service. They require a ‘light’ version of a health economic assessment by the globally recognised National Institute of Health and Care

The companies that are providing these internet enabled therapy sessions generally offer computerised CBT - including IESO (a British clinically-led company), Silvercloud (an Irish company that scaled well in IAPT and was bought by US giant Amwell in 2021) and Wysa (founded in India, now headquartered in Boston, and available in over 65 countries).

If you’re interested in providing internet enabled therapy, you should take a look at:

The Digitally Enabled Technologies criteria

NICE’s existing Early Value Assessments for digitally enabled therapies for anxiety and depression

The Digital Technologies Assessment Criteria (DTAC) - which is relevant to pretty much any digital technology selling into the NHS

Efficiency-focused services and platforms

Some companies have chosen not to go down the digitally enabled technology route for fears that they’d have to overfit their products to serve this market. Remember, one of the foundations of this service was consistent data collection and the involvement of highly trained practitioners - meaning your technology needs to tick the system’s boxes.

Alternatively, the other ways of scaling around Talking Therapies include more of a service / platform play than a treatment play. Mayden provide a bespoke electronic patient record for psychological therapies, called iaptus. You can also check out our deep-dive on Limbic, who are using AI to work on the supply and demand problem in Talking Therapies.

2. National Services

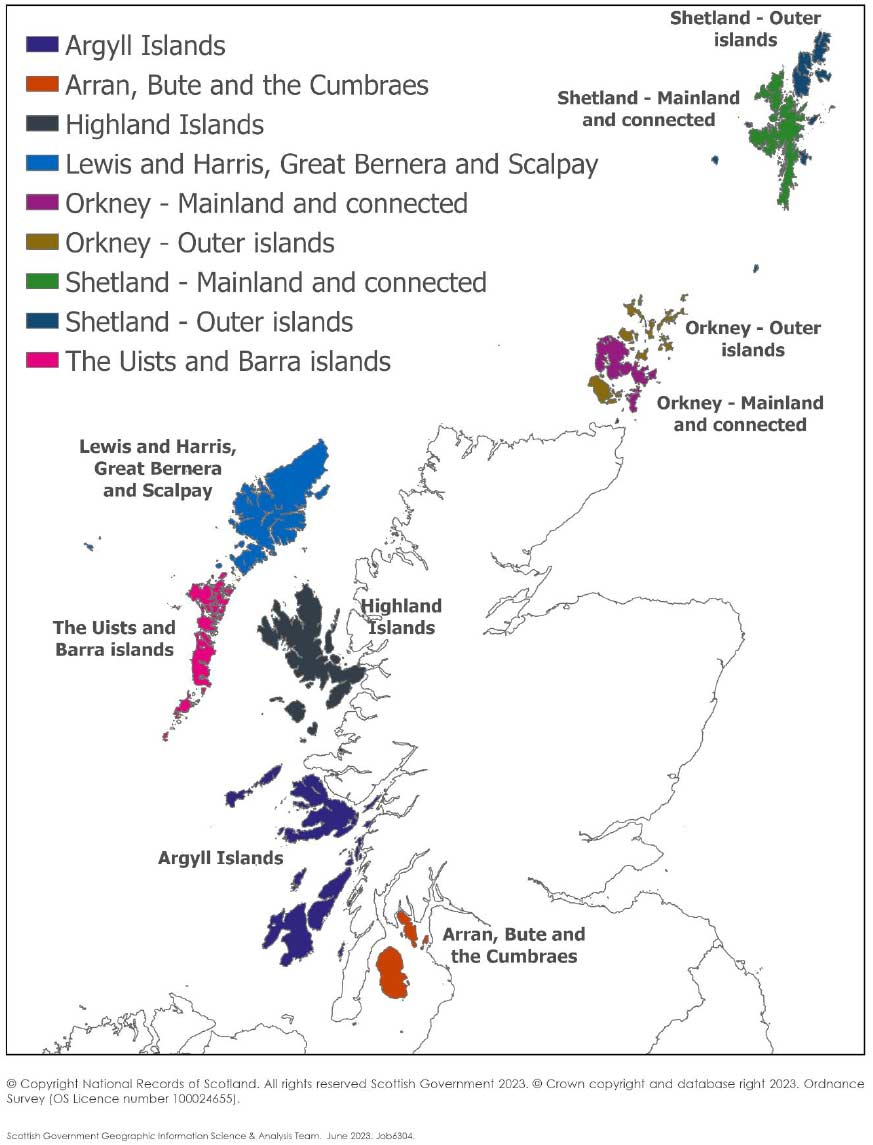

The most elusive customer is the one that gives you access to all the patients in a nation. Whilst England, Wales and Northern Ireland lack a centralised process for digital mental health companies to drive revenue and patient adoption at a national scale, Scotland (population c. 5m) tells a different story.

Like most countries, the Scottish Government was looking for a way to improve accessibility, reduce waiting times, and provide scalable mental health support. Where England landed on the practitioner-led Talking Therapies model, you could argue that Scotland instead came to the Digital Mental Health Programme.

The Digital Mental Health programme intends to address the increased demand for mental health services by maximising the impact of technology, ensuring sustainability and expansion of digital services while creating an environment of collaboration across stakeholders and relevant areas within Scottish Government.

It’s worth noting that a tech-led programme makes sense when you look at the geography of Scotland - which has a lot of islands. For example, the islands of Barra and Vatersay are home to about 1,300 people who at one point had no permanent doctor, and faced a six-hour drive or one-hour flight to their nearest Accident and Emergency centre. Being able to offer equity of access means a lot more openness to digital innovation (and some creative thinking on how to reduce digital exclusion!).

Working with the Scottish Government requires proving that your solutions meet the right evidence standards, can be implemented in line with their needs, and proving in the real world that you can deliver equitable access, starting with access in selected, diverse areas. Companies with traction within the programme include Big Health, Silvercloud (again) and IESO (again).

3. Local NHS / Government

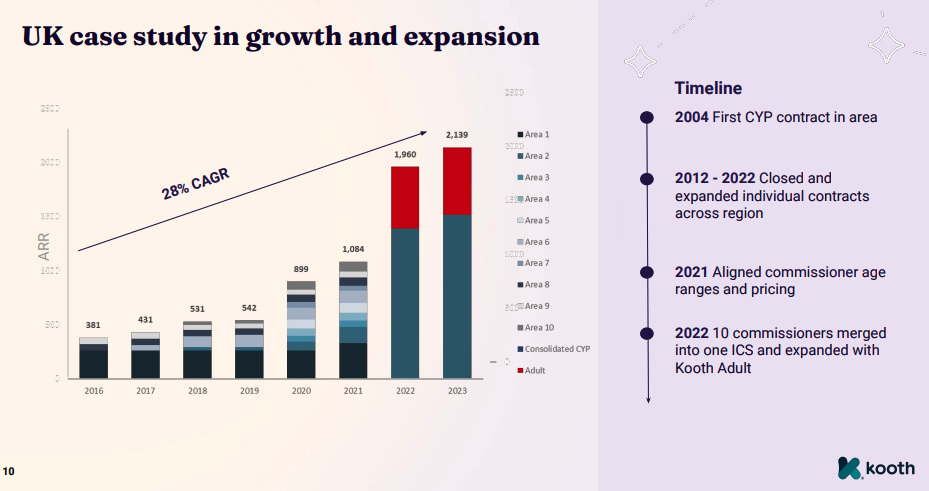

A theme you might be picking up is that when you’re selling into the public sector, you might end up with more than one type of buyer. A great example of this is Kooth, a UK mental health tech company focused on children and young people (we did a deep-dive on them too).

Using public tender data from Tussell, we can see that of their 51 successful public sector procurements since 2020, 75% were with Local Government (example award from Devon County Council) or Integrated Care Boards (example award from Frimley ICB).

A look back at their investor presentations over this same period reveals a similar dual focus on the NHS and local government, especially in their early stages, before they started focusing more on the US.

Year | NHS | Local Government |

2020 | 85% of English commissioners | 30/32 London boroughs |

2021 | 90% of English commissioners 60% of Welsh commissioners | 32/32 London boroughs |

2022 | Speaks about an increase in access to 8.8m adults | No reference to boroughs |

2023 / 24 | Speaks about focus on retaining existing contracts and policy advocacy |

Reaching Integrated Care Boards isn’t a straightforward or single path, and we’ll get into this more in Chapter 2. In many ways, reaching an ICB is the result of scaling up existing relationships at sub-ICB level as the Kooth case study below shows.

Kooth Case Study

4. Selling to businesses

Because mental health care is available to the UK public for free, the market for B2B services is a relatively small portion of the overall spend (approx. £118m).

However, like many other developed countries, there has been consistent growth in this market, growing at a 7% CAGR since 2003. Due to the supply-demand and waitlist problems in the NHS, many organisations offer some level of mental health support to their employees through a private EAP service.

Unmind is a leading UK business operating as a workplace mental health platform. They provide core EAP services (including crisis care) as well as therapy, coaching (by humans and AI), content resources, insights and more. They’ve had success selling to large organisations like Uber, Diageo and Standard Chartered.

B2B Mental Health services is still a small market in the UK but it’s also relatively competitive, making it a difficult market for international businesses to enter.

5. Going D2C

When it comes to D2C as a commercialisation option for Mental Health services, the UK is similar to most other developed nations - difficult to make work at scale, possible for niches and a helpful tool for landing large payer contracts. In particular - the presence of the NHS changes how people approach paid-for mental health apps.

Ariana Alexander-Sefre is the founder of Spoke, a company focusing on meeting young people (and especially men) where they already are, by improving mental health through music. Ariana has dug deep into the research on paywalls and culture, the differences between the UK and other countries and how that impacts D2C strategies in the UK.

In the US, it’s easier to put a paywall at the start of the user journey, and people would be happy to start a 7 day free trial. In the UK - if someone automatically has a paywall, and you can’t test out what it’s about, you delete the app and don’t go further.

This is just one example of cultural differences businesses should be aware of, especially if pursuing a D2C strategy.

Alternatively, some companies have tried the B2C2B route as a pathway to larger, public contracts in the UK. For example, Flow Neuroscience had initial success selling direct to consumers across Europe, including in the UK. In fact, their D2C success in this market helped them land their initial NHS Trust contracts.

Other interesting D2C players in the UK include Mettle, a “mental fitness toolkit for men” co-founded by Bear Grylls, and US D2C offerings like Headspace and Calm have had success in the UK market.

While the UK economy is far from booming, there are still large numbers of affluent people - especially in metro centres like London - with disposable income and a willingness to spend on health and wellness services.

A quick note on regulation and evaluation

When it comes to regulated tech, it’s worth remembering the foundations of the NHS - being good for patients, good for clinicians and good for taxpayers. The UK, compared to other markets, is especially focused on evidence-based decision-making and cost-effectiveness. This is reflected in the standards it holds for evaluation and adoption in particular - from obtaining NICE guidance to the value proposition you take to the public sector.

The types of bodies you might engage in the course of entering the UK market include:

MHRA (Medicines and Healthcare products Regulatory Agency): Oversees the regulation of medical devices, ensuring they meet safety and performance standards.

Care Quality Commission (CQC): Regulates and inspects health and social care providers, including those delivering digital health services.

UK Information Commissioner’s Office (ICO): Regulates data privacy under GDPR, critical for mental health tech managing sensitive personal data.

NICE (National Institute for Health and Care Excellence): Evaluates the clinical and cost-effectiveness of health technologies and provides guidance for NHS adoption.

If you’re serious about the UK market it’s worth engaging a local team who can help based on your product and pathway positioning - one example we’re aware of is Hardian Health.

OK, that concludes Part I of our Guide to the UK Mental Health Market.

We really hope you found this useful. Part II will be released in the coming weeks where we’ll share more insights from leaders on the trends shaping this important market right now.

That’s all for this week.

Remember to contribute to our founder and operator survey. Otherwise, see you back here next week!

Keep fighting the good fight!

Steve

Founder of The Hemingway Group

P.S. feel free to connect with me on LinkedIn

P.P.S. If you want to become a THR Pro member, you can learn more here.